Nutana, Saskatchewan: A Riverside Legacy

By Jules Torti @ Realtor.ca

April 6, 2020

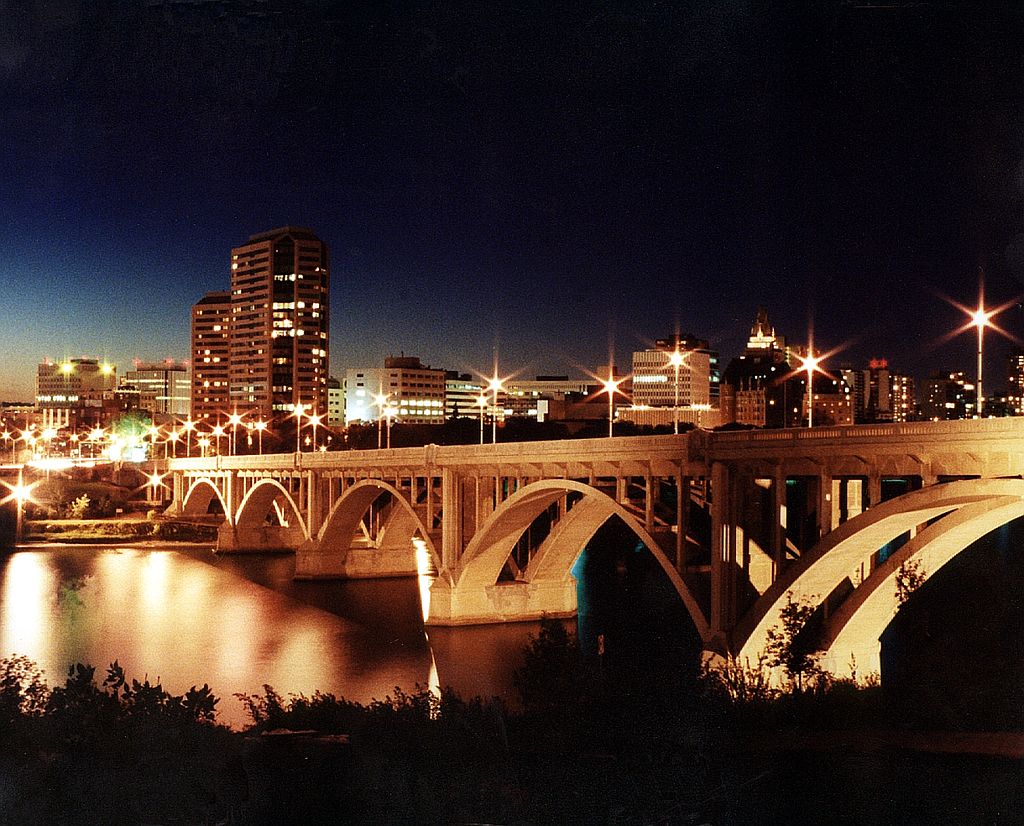

Nutana is an affordable, gentrified neighbourhood conveniently located near the hustle of Saskatoon, Saskatchewan. The main artery and cultural heartbeat is found along Broadway Avenue. Bounded by 8th Street to the south, Clarence Avenue to the east and the South Saskatchewan River to the west, Nutana’s grid system is fool-proof. Avenues run north to south and streets run east to west. In 2019, the area was home to 6,158 residents — a modest jump from the mere 70 people who lived here in 1883.

Did you know?

- The Broadway Theatre is Canada’s only community-owned non-profit repertory cinema. The 430-seat venue has a rotating lure of date night options including arthouse films, live music, theatre and dance. To boot, its 88 solar-panel array (the third largest in the province) is expected to generate 50% of the building’s electricity needs.

- At nearby Black Fox Farm and Distillery, the cut-flower farm grows 90% of the ingredients necessary for their gin, liqueur and vodka production. Canada’s preeminent on-farm distillery is a wink back to the Temperance Colonization Society, a group of Toronto Methodists who were the first to permanently settle here. Black Fox’s Gin #3 is a marriage of 15 different spices and flowers with floral notes of calendula flowers and rhubarb.

- Urdu, or Lashakri, the official national language of Pakistan, is the second-most prevalent language spoken in Nutana, after English (2016 Census).

Housing market

The heritage-rich riverside neighbourhood is considered a middle to upper-income area, with a median personal income of $47,870, and a homeownership rate of 51.5%. In 2017, Nutana was ranked No. 1 on rentfaster’s Most Popular Saskatoon Neighbourhoods to Live In because of its modern vibe, energy and spotless beauty. In 2019, stats from the City of Saskatchewan, Assessment and Taxation indicated a single-family dwelling average of $541,668 while low-rise apartment condos reached $315,107 (2016 census). According to 2019 MLS data, the average sale price of a home was $467,841.

Where to live

The newest coveted address is the Escala development (2020). The two or three-bedroom floor plans offer 1,088 square-foot balconies with uninterrupted river and city views. Nutana’s proximity to the University of Saskatchewan means it’s a hotbed for student rentals. College Quarter residences are located here due to a high walkability score, pub scene and easy access to several bus routes.

What to do

- A visit to the Marr Residence, a national historic site, is a genuine treat for architecture addicts. Built in 1884 for stonemason Alexander Marr as part of the Temperance Colony, it was a two-storey pioneer dream home with a mansard roof and hardwood floors. The house served as a temporary field hospital after the Battle of Fish Creek.

- Though Saskatoon is better known for its spudnuts (potato doughnuts), shishliki (marinated lamb skewers), pickerel cheeks and Saskatoon Berry Pie, why not grab a pint of Sumac Hazy Pale Ale from the local, High Key Brewing, at the Yard & Flagon on Broadway (Saskatoon’s first rooftop patio)? Try the provincially iconic jerk dry ribs and fried pepperoni chips (served with cheddar cheese and pizza sauce).

- Don’t miss the annual Meewasin Pelican Watch (March). Guess the date and time of the first pelican to touch down between the CPR Bridge and The Weir to win a $500 prize pack! Once endangered, the pelicans have graced the South Saskatchewan River since the late 1970s.

Source: https://www.realtor.ca/blog/postpage/12448/1364/nutana-saskatchewan-a-riverside-legacy

.png)

Why: To avoid mold and water damage to the bones of your house.

How: It’s as simple as grabbing a flashlight, crawling in there and taking a close, careful look. Pay attention to corners, edges and changes in color, and use your fingers to test for dampness if you aren’t sure. If you find any water, call a home inspector immediately to figure out where it’s coming from.

When: Every fall before it rains. The key is to fix existing water damage before any more water gets in.